Miami Cash Home Buyers Double the National Average

According to the Miami Association of Realtors, total Miami luxury home sales rose 24.1 percent year-over-year in May as existing condominium sales rose for the second consecutive month.

Total Miami luxury sales ($1 million-and-above) increased from 158 to 196 in May 2018, a rise of 24.1 percent. Condo luxury sales led the surge by posting a 58.6 percent jump (from 58 luxury transactions in May 2017 to 92 last month). Condo and single-family $1 million-and-above transactions have each now increased year-over-year in four of the last five months.

"Miami real estate luxury sales continue trending upward," MIAMI Chairman of the Board George C. Jalil said. "Strong pent-up demand for $1 million-and-above Miami properties, sellers becoming more reasonable with their prices and the federal tax reform leading more home buyers from high-taxed northern states to purchase in Florida, which has no state income tax, are several key factors."

Miami Condo Sales Increase for Second Consecutive Month

Miami existing condominium sales increased 0.6 percent year-over-year in May 2018, rising from 1,384 to 1,392. The increase comes on the heels of a strong April 2018 which saw condo transactions jump 24.6 percent.

Total Miami home sales decreased 3.9 percent year-over-year, from 2,728 to 2,622. Miami single-family home sales decreased 8.5 percent in May 2018, from 1,344 to 1,230. The decrease is due to a lack of inventory in lower price points. Inventory decreases for Miami single-family homes selling at $400,000 and below.

Total sales volume increased to $1.3 billion from $1.2 billion in May 2017.Existing condos saw the biggest increase, rising from $517.9 million total sales volume to $645.8 million (an increase of 24.7 percent). Single-family home total dollar volume rose 3.4 percent, from $651.2 million to $673.6 million.

Lack of access to mortgage loans continues to inhibit further growth of the existing condominium market. Of the 9,307 condominium buildings in Miami-Dade and Broward counties, only 12 are approved for Federal Housing Administration loans, down from 29 last year, according to Florida Department of Business and Professional Regulation and FHA.

6.5 Consecutive Years of Price Appreciation in Miami

Miami-Dade County single-family home prices increased 7.7 percent in May 2018, increasing from $325,000 to $350,000. Miami single-family home prices have risen for 78 consecutive months, a streak 6.5 years. Existing condo prices rose 8.9 percent, from $225,000 to $245,000 in May. Condo prices have increased in 81 of the last 84 months.

Low mortgage rates makes purchasing a home more affordable. According to Freddie Mac, the average commitment rate for a 30-year, conventional, fixed-rate mortgage increased for the seventh straight month to 4.59 percent in May (highest since 4.64 percent in May 2011) from 4.47 percent in April. The average commitment rate for all of 2017 was 3.99 percent.

Miami Distressed Sales Continue to Drop, Reflecting Healthy Market

Only 6.4 percent of all closed residential sales in Miami were distressed last month, including REO (bank-owned properties) and short sales, compared to 10.0 percent in May 2018. In 2009, distressed sales comprised 70 percent of Miami sales.

Total Miami distressed sales declined 38.3 percent year-over-year, from 274 to 169 last month.

Short sales and REOs accounted for 1.3 and 5.1 percent, respectively, of total Miami sales in May 2018. Short sale transactions dropped 52.1 percent year-over-year while REOs fell 33.5 percent.

Nationally, distressed sales accounted for 3 percent of sales (lowest since NAR began tracking in October 2008), down from 5 percent a year ago.

Miami Real Estate Selling Close to List Price

The median number of days between listing and contract dates for Miami single-family home sales was 44 days, an 8.3 percent decrease from 48 days last year. The median number of days between the listing date and closing date for single-family properties was 92 days, a 6.1 percent decrease from 98 days.

The median time to contract for condos was 73 days, a 2.7 percent decrease from 75 days last year. The median number of days between listing date and closing date decreased 2.6 percent to 112 days.

The median percent of original list price received for single-family homes was 96.0 percent. The median percent of original list price received for existing condominiums was 93.3 percent.

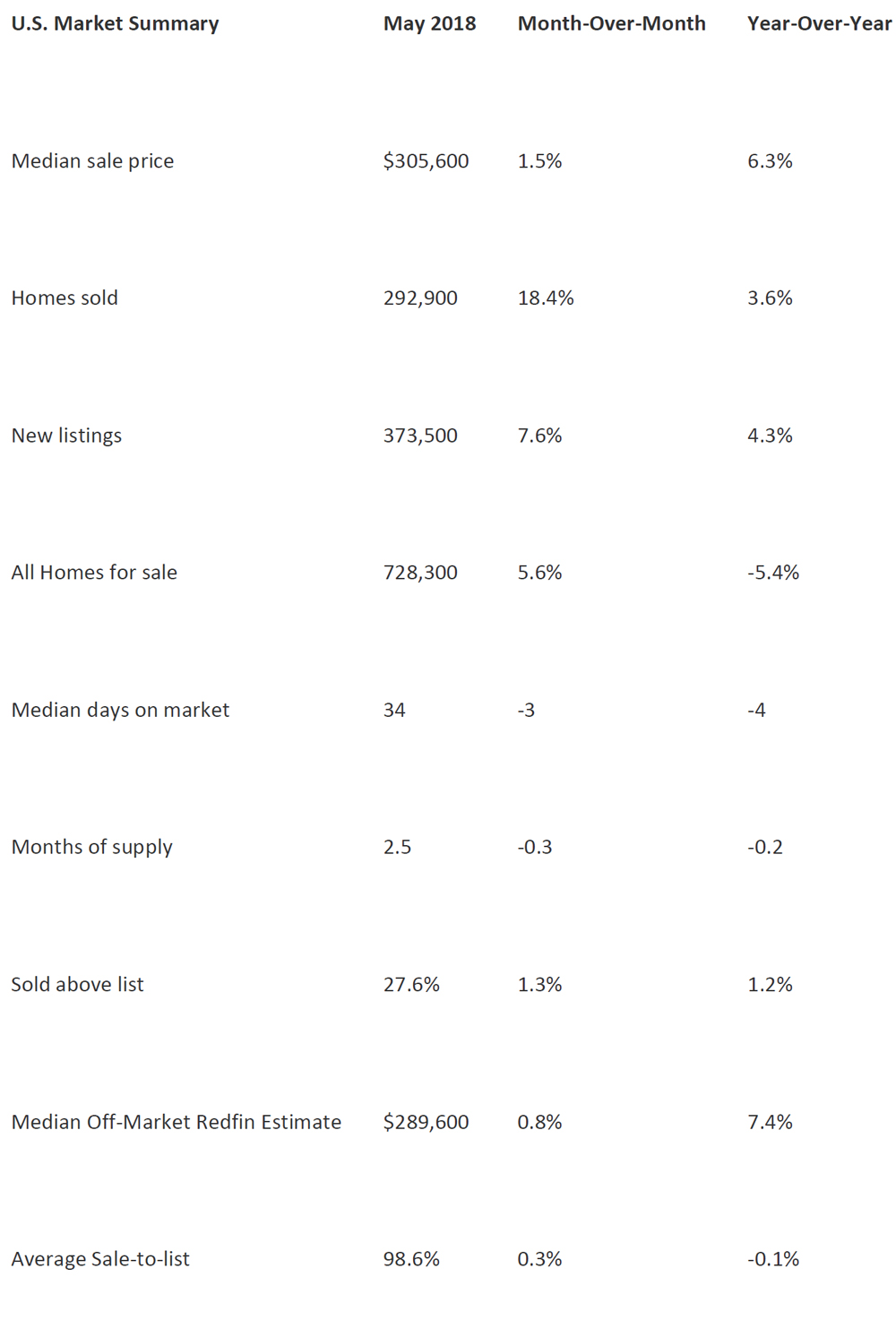

National and State Statistics

Nationally, total existing-home sales decreased 0.4 percent to a seasonally adjusted annual rate of 5.43 million in May from downwardly revised 5.45 million in April. With last month's decline, sales are now 3.0 percent below a year ago and have fallen year-over-year for three straight months.

Statewide closed sales of existing single-family homes totaled 28,071 last month, up 0.8 percent compared to May 2017, according to Florida Realtors. Statewide closed condo sales totaled 12,012 last month, up 4.1 percent compared to a year ago.

The national median existing-home price for all housing types in May was $264,800, an all-time high and up 4.9 percent from May 2017 ($252,500). May's price increase marks the 75th straight month of year-over-year gains.

The statewide median sales price for single-family existing homes was $255,000, up 6.7 percent from the previous year, according to Florida Realtors. The statewide median price for townhouse-condo properties in May was $188,688, up 6 percent over the year-ago figure.

Miami's Cash Buyers Represent almost Double the National Figure

Miami cash transactions comprised 39.0 percent of May 2018 total closed sales, compared to 39.4 percent last year. Miami cash transactions are almost double the national figure (21 percent).

Miami's high percentage of cash sales reflects South Florida's ability to attract a diverse number of international home buyers, who tend to purchase properties in all cash. Miami has a higher percent of cash sales for condos due to lack of financing approvals for buildings.

Condominiums comprise a large portion of Miami's cash purchases as 50.9 percent of condo closings were made in cash in May compared to 25.5 percent of single-family home sales.

Balanced Market for Single-Family Homes, Buyer's Market for Condos

Inventory of single-family homes increased 0.4 percent in May from 6,195 active listings last year to 6,219 last month. Condominium inventory increased 2.2 percent to 15,502 from 15,326 listings during the same period in 2017.

The increase in inventory is for properties above $400,000. The market had a 3.5 percent jump in properties listed for $400,000 to $599,999 in May 2018, 4.4 percent for $600,000 to $999,999, and 3.4 percent for $1 million and above.

Miami saw a drop in inventory for properties below $400,000.

Monthly supply of inventory for single-family homes increased 7.1 percent to 6.0 months, which indicates a balanced market. Existing condominiums have a 14.1-month supply, which indicates a buyer's market. A balanced market between buyers and sellers offers between six and nine months supply of inventory.

Total active listings at the end of May increased 0.92 percent year-over-year, from 21,521 to 21,721. Active listings remain about 60 percent below 2008 levels when sales bottomed.

New listings of Miami single-family homes decreased 0.4 percent to 1,881 from 1,888. New listings of condominiums increased 8.1 percent, from 2,431 to 2,617.

Nationally, total housing inventory at the end of May climbed 2.8 percent to 1.85 million existing homes available for sale, but is still 6.1 percent lower than a year ago (1.97 million) and has fallen year-over-year for 36 consecutive months. Unsold inventory is at a 4.1-month supply at the current sales pace (4.2 months a year ago).